Three key levers for improving telco B2C margins

A new report from McKinsey & Company argues telco operators need to think like ServCos to raise profits.

Telecom operators have created enormous value with new applications and services, but have underperformed shareholders' expectations. Some operators are separating their network operations (NetCo) from customer-facing operations (ServCo) to expose the value of their network assets or attract external investment to fund expansion.

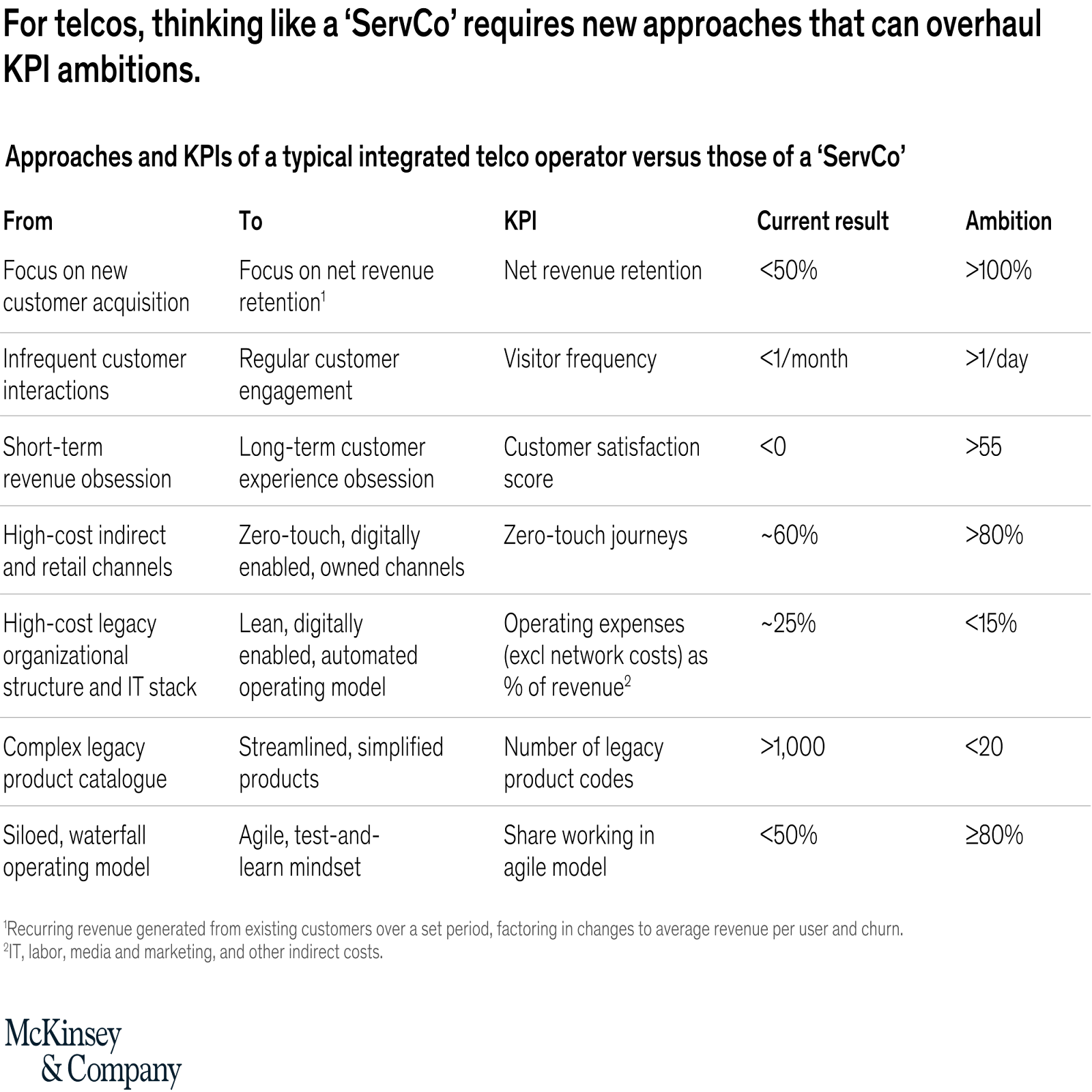

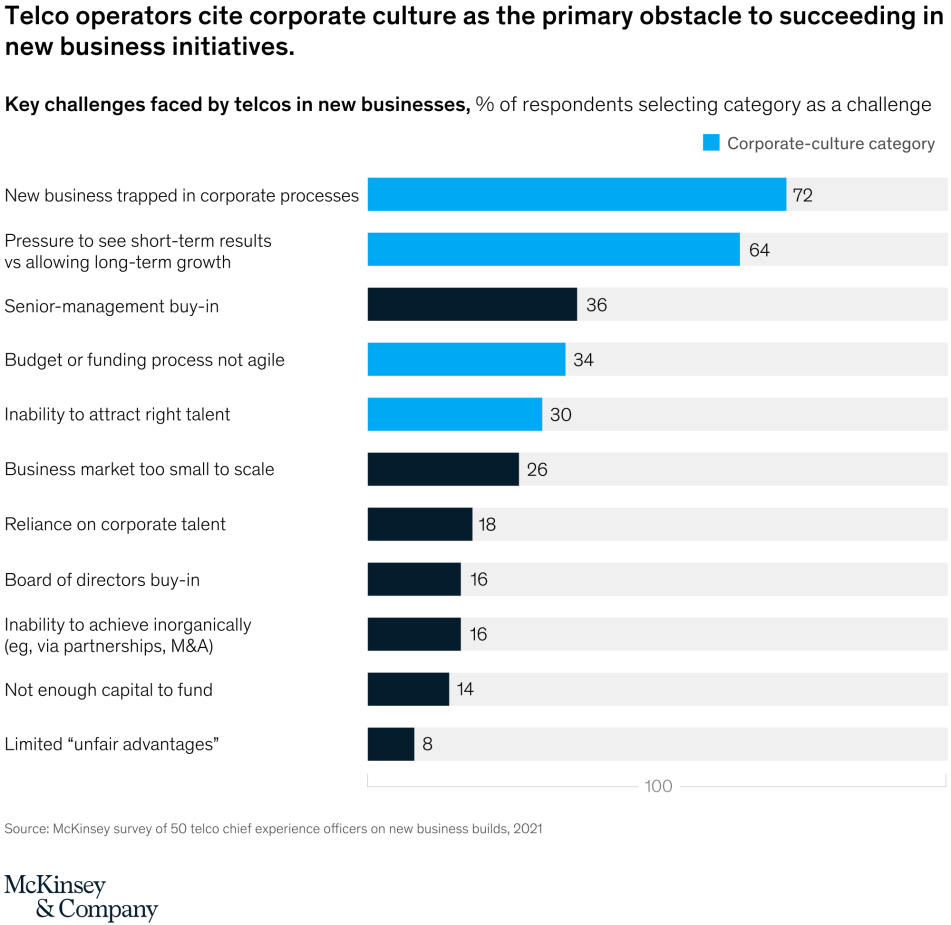

Telco leaders have not fully embraced the necessary scale of transformation to succeed in a hypercompetitive environment. Integrated telcos can accelerate transformation by adopting the mindset of a ServCo.

Adopting the ServCo mindset can help operators focus on existing customers and reduce negative market price dynamics. Telcos can quadruple the valuation of their business-to-consumer (B2C) operations by improving margins and implementing multiple re-ratings. Three key levers can help telcos improve margins: driving value from core connectivity, using data to create new products and services, and enhancing customer experience.

By adopting the mindset of a ServCo, B2C leaders of integrated telcos can accelerate their transformation and compete more effectively in the hypercompetitive telecom industry. The ServCo mindset can help operators shift from legacy practices that focus on short-term revenue to strategies that generate longer-term customer value and satisfaction. This can also make new revenue streams more attractive by reducing margin dilution.

Additionally, lower margins will force operators to focus on existing customers and reduce the negative market price dynamics caused by acquiring new customers with deep discounts.

To fully embrace the ServCo mindset, telcos will need to define a clear vision for how they will compete without the benefit of network differentiation which will involve pursuing the three key levers. Each lever will require bold moves and fundamental shifts, but the potential rewards are significant. By implementing these levers, telcos can improve their B2C margins and raise their valuations.

To drive value from core connectivity, telcos can optimise their existing connectivity business by increasing average revenue per user (ARPU) through customer value management and cost reductions. This can be achieved by offering personalised packages and bundles, implementing data-driven pricing, and reducing operational costs through automation and standardization.

The second lever involves using data to create new products and services. Telcos can leverage their unique data assets, such as usage data, location data, and customer profile data, to develop personalised offers and services that meet the needs of their customers. This can include offering data-driven services such as location-based advertising and personalised health services.

The third lever is enhancing customer experience. Telcos can improve customer satisfaction and loyalty by providing seamless and convenient experiences across all customer touchpoints, such as online, offline, and social media. This can be achieved by implementing customer-centric design, leveraging customer feedback, and providing personalized support through chatbots and other digital channels.

By pursuing these three levers, telcos can improve their B2C margins and increase their valuations. This will require a significant transformation and a willingness to embrace bold changes, but the potential rewards make it a worthwhile pursuit.

In addition to pursuing these three levers, telcos can also consider implementing structural or legal separation to fully capture the value of their network assets and support their growth. This can involve creating a separate NetCo and ServCo, with the NetCo responsible for network operations and the ServCo focused on customer-facing operations. This separation can allow NetCo to attract external investment to fund network expansion, whilst ServCo can focus on driving growth and maximizing value.

However, implementing structural or legal separation is not a decision to be made lightly. It requires careful planning and consideration, as it can be a complex and costly process. Telcos should carefully weigh the potential benefits and drawbacks of separation before making a decision.

Overall, adopting the mindset of a ServCo and pursuing the three value-creating levers can help telcos accelerate their transformation and compete more effectively in the hypercompetitive telecom industry. By improving their B2C margins and increasing their valuations, telcos can reignite growth and reimagine their capabilities to better meet the needs of their customers.

Without the shield provided by network margins, B2C telco leaders face a dramatically different economic reality. Suddenly, margins drop to between 5% and 15%, from 30% to 40%, casting cost cuts and revenue growth as stark imperatives.

Depending on how many levers an operator chooses and how they execute these choices, it’s possible to raise B2C margins, including a true accounting of network costs, to between 15% and 25%, up from 5% to 15%.

Examples already exist of integrated telecom operators that have succeeded in driving cost reduction and revenue growth through a customer lifetime value-based approach, beating out organisations that have moved more slowly and might benefit from the accelerant that a ServCo lens provides.

PT Telekomunikasi Selular (Telkomsel) transformed its core connectivity with new offers for underserved customers, seamless digital channels, a separate digital native brand, and a data analytics platform incorporating 9,000-plus data points per customer.

The MyTelkomsel app now gives customers tailored offers, real-time views of data usage, and easy payment options. It has close to 30 million monthly active users, a tenfold increase over the previous app. Veronika, Telkomsel’s chatbot, handles 97% of customer inquiries made through the app, as well as driving incremental revenues from phone credits and data packages.

To appeal to digital natives, Telkomsel launched by.U, a fully digital brand. In record time, its cross-functional team created and refined a platform that allows users to select a prepaid SIM card that arrives at their doorstep, activate their numbers remotely, manage top-ups and quotas, and make payments. To ensure that innovation continues after launch, by.U adopted an agile organisational structure. The brand reached its one-year customer acquisition goal in nine months. Within 15 months, it had nearly two million subscribers and a market-leading customer satisfaction score.

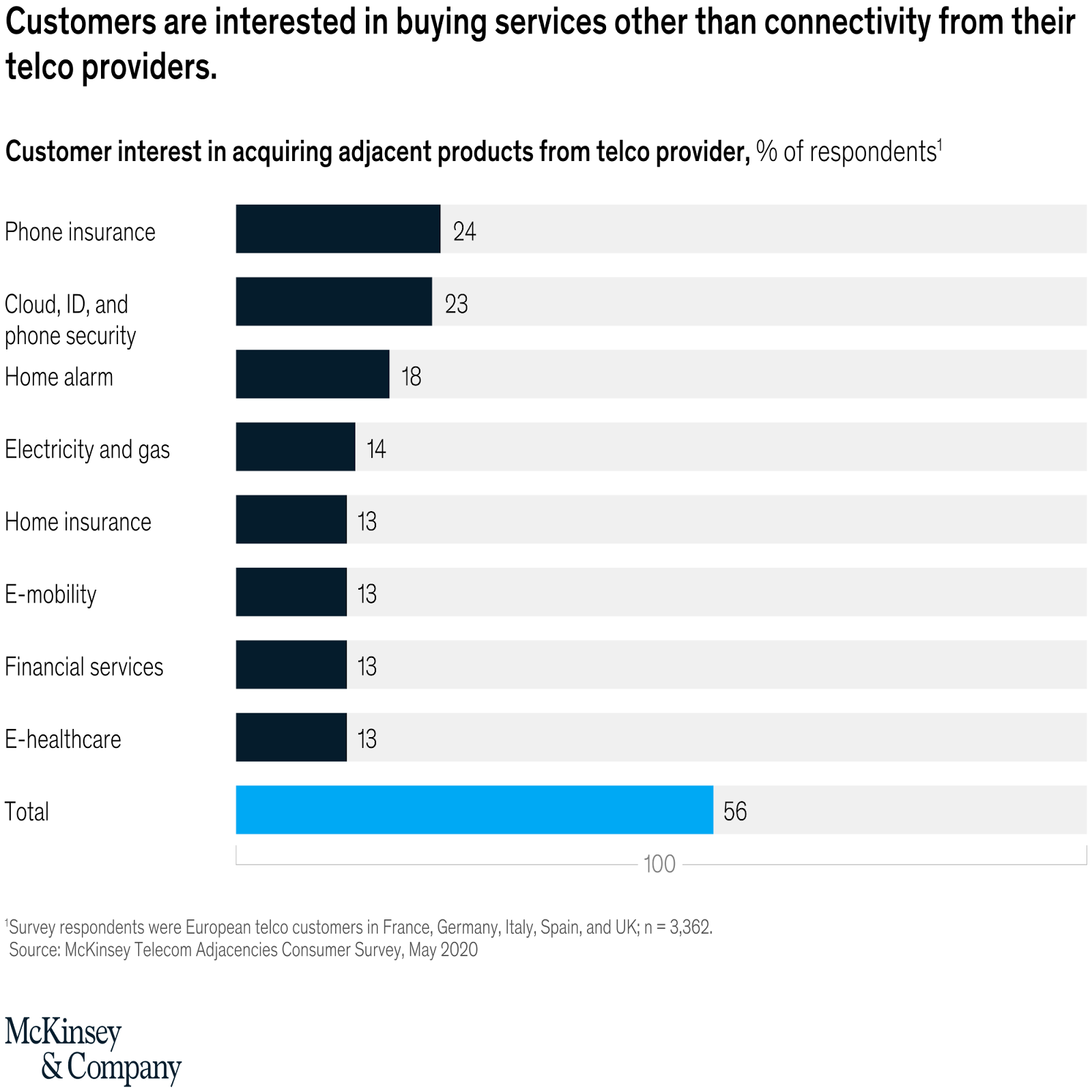

Around 56% of European customers say they would buy a service other than connectivity from their telco provider. Customers express the highest willingness to purchase phone insurance and products related to cybersecurity and home security, followed by products related to energy, healthcare, and financial services.

Norway’s Telenor has unlocked growth by expanding into mobile phone insurance and security and privacy offerings. A prime example is its SAFE product, which provides protection against identity fraud and personal data theft. Since SAFE was released in 2020, it has attracted some 300,000 users who are willing to pay nearly $13 a month extra for the service.

SAFE has met customers’ desire for greater security protections and was directly integrated into the My Telenor app to facilitate the easiest access and payment. Telenor credits SAFE with reducing churn, increasing customer loyalty, and further driving top-line growth. Overall, adjacencies are responsible for two-thirds of Telenor Norway’s ARPU increase between 2017 and 2020.

In Spain, Telefónica acquired 50% of the alarm business of leading home-security player Prosegur rather than trying to build a new proposition in-house, combining its own distribution channels and customer base with Prosegur’s highly regarded product and brand. The resulting business, the country’s first to offer 24/7 intervention services in response to a triggered alarm, was critical to Telefónica’s success in growing its home-security customer base to 406,000 customers since launch, including roughly 60% year-on-year growth in the first half of 2022.

However, telecom operators have historically struggled to scale adjacency plays. Roughly 75% of these new businesses have yet to reach $100m in revenues, and around half are achieving less than 10% profitability.

NTT DOCOMO has built a robust ecosystem offering digital content, healthcare expertise, financial services, and a B2C marketplace. The ecosystem was responsible for 23% of the operator’s revenue in the fiscal year 2021. The telco has relentlessly pursued innovation in customer experience while building its ecosystem; in 2021, it had the highest number of AI-related patent submissions in Japan. It has inspired cross-product engagement through its d POINT CLUB rewards program, in which customers earn points by purchasing products and services from ecosystem players.

Strategic investments and partnerships have been critical as NTT DOCOMO has ventured into new verticals. It has built out healthcare and telemedicine solutions through partnerships with Genova Diagnostics, Medley, and OMRON Healthcare. It partnered with ORIX to launch a ridesharing service and with THEO to offer an AI-driven investment advisory. It integrates video services from several partners, including DAZN, Disney+, and Hikari TV.

The European telco landscape is highly fragmented, with 87 customer-facing entities catering to more than one million subscribers each. In the United States, by contrast, there are only 16.

If the European market were served by a total of 16 B2C telecom platforms, the same number as in the United States, and operators were able to reduce their B2C IT-related operating expenses and capital expenditures by half, this would save more than $5 billion a year.

Octopus Energy, a renewable-energy retailer, has scaled internationally by licensing the Kraken technology platform that it built for UK B2C operations to partners in nine countries. The Kraken platform hosts the entire customer service operation, manages disaggregated energy sources, communicates with industry bodies, and uses tools such as machine learning to offer dynamic tariffs. Revenues from these licensing arrangements grew by 584% in 2021.

Companies that have made the switch have saved more than $100m in 2021. In 2022 alone, Origin Energy is expected to save as much as $80m.

This is a summary of the report issued by McKinsey & Company.